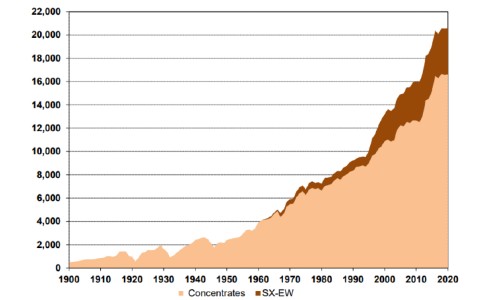

Copper is one of the few raw materials which can be recycled repeatedly without any loss of performance. Recycling, innovation and mining exploration continue to contribute to the long-term availability of copper. Since 1900, global copper mine production has grown by 3.2% per annum to 20.6Mt in 2020. Chile contributed to almost one-third of the world copper mine production in 2020, followed by Peru 10%, China 8.3%, Congo 6.3% and US 5.8%. Kazakhstan is the world’s 10th largest copper mine producer.

The global copper market is expected to be in a mild deficit of 82,000 tonne in 2022 (or at less than 1% of global copper consumption), supported by the recovery in global copper demand and ESG agenda.

The IMF projects that (i) global demand/consumption of critical energy transition metals will increase in the long-term up to 2030s (copper by a factor of 2x), (ii) global demand for metals will be frontloaded between now and 2030, driven by the need of large initial investments for the switch from fossil fuels to renewables – implying global metals play up to 2030s.